China's Invasion of Taiwan

China's Invasion of Taiwan

Why it is likely, and what the commercial impact will be.

Executive Summary

It is likely that, in Xi Xinping’s eyes, Russia’s invasion of Ukraine was a great success for Putin, worth emulating. Xi would benefit from a carefully managed military crisis around Taiwan, as it would help him assess the US’ reaction and China’s vulnerabilities, identify domestic enemies, and push forward a Chinese rejuvenation programme.

China has no reason to start with an amphibious landing on Taiwan, but rather with efforts to cut off Taiwan’s trade, and to escalate to full-scale conflict.

In the likely event of a Chinese invasion of Taiwan, the EU would likely follow the US’ lead, and, along with the US, sanction China very aggressively in a way comparable to Russia. China would respond with asset expropriations and sanctions of its own.

This will herald the end of Western led globalisation, leading to two rival camps, a China – Russia – Iran led camp that uses the yuan and barter, and a US-led camp that uses a rapidly inflating dollar.

The US dollar cannot be a truly global reserve currency if the US sanctions the world’s largest manufacturer – China – and the world’s largest food and energy producer – Russia. It may remain an important reserve currency, and the reserve currency of the West, however.

In such circumstances, European exports to the rest of the world would fall dramatically. Europe would be struggling with uncompetitive energy prices, high labour costs, and a greater regulatory burden. US exporters would fare better due to cheaper energy costs and the possibility of de-regulation under a Trump administration.

China’s larger industrial base will likely make it more resilient in a war than the West. China will benefit from lower energy and food costs due to its alliance with Russia and Iran, enabling it to improve its export position.

Supply chain disruption, due to war and to sanctions, will be unprecedented. The extent of disruption will in part depend on whether North Korea seizes the opportunity created by a Taiwan invasion to move against South Korea. This would likely make supply chains dependent on Japan and South Korea far more fragile.

The West would likely be plunged into a political crisis due to falling living standards and the discrediting of the ruling classes.

Companies with supply chains focused on Morocco, Türkiye and South America would fare better than those with supply chains focused on East Asia. Countries that can continue trading with both blocs also stand to benefit.

Analysis

Xi’s perspective

Putin successfully boosted Russia’s military industrial base, while deterring the West from fighting Russian forces directly. Russia is outproducing NATO in terms of tanks, ammunitions and other ordnances, and maintains a significant firepower advantage over Ukraine. The sanctions on Russia forced it to increase its self-reliance, and its reliance on allies. The war was an excuse to discipline dissident oligarchs with deep ties to the West, forcing them back in line. Recall that oligarchs are always the main threat facing a leader, as they are well-financed and capable of challenging him in ways that the public are not. Furthermore, sanctions against Russians in general forced Russian oligarchs to move their wealth away from the West and back to Russia or countries friendly with Russia. Western sanctions forced these oligarchs to re-orient their businesses towards neutral or friendly country. The overall result is a major reduction in Western influence over Russia.

Russia is therefore now more autonomous, with Putin in an increasingly unassailable position. Xi would likely view such an outcome as good for China, as a means of securing China’s influence over the rest of the world excluding the West, and as a means of cementing his own rule. While an invasion of Taiwan, and adjusting to subsequent conflict and sanctions, would be economically costly and very risky, it may be necessary strategically and politically.

Consider that those who are rich and weak do not remain rich for long, but those who are poor and strong can quickly become rich. Nations place security above economic interests. The US and China are locked into a cycle where China increases its military capability, which China views as a legitimate reaction to Western interference, and the US increases its financing and arming of Taiwan, which the West sees as necessary deterrence in the face of China’s arms build-up. This dynamic makes it more likely that China will conclude that war with Taiwan is the only answer.

China and its allies

The best bet for the Iran – Russia – China – North Korea axis is to impose a series of escalating crisis – as Russia advances in Ukraine, due in large part to Ukraine’s manpower shortages and inability to effectively defend its skies – Iran is escalating in the Middle East. Following the Iranian escalation, which will help deplete the US’ limited stocks of key military assets such as ship-based air defence missiles, it would make sense for China to also escalate. This would be especially so the longer the Israel – Gaza war continues – and with it the conflict in the Red Sea – and the greater any subsequent Iran – US escalation. It is worth recalling that the IRC axis is seeking to overthrow the existing US-led order and replace it. They are likely to pursue a cooperative, coordinated approach.

Crisis and its benefits

The purpose of China is not limited to capturing Taiwan. The purpose of China is a new world order, in which Taiwan is a part of the prize. That world order can include Chinese hegemony, or a Chinese sphere of influence. But it cannot include the US on China’s doorstep threatening to choke off its ports.

The US wants to keep China within the first island chain. China needs to go beyond the first island chain and consolidate its holdings in the South China Sea.

A crisis around Taiwan can be the catalyst for Xi to rejuvenate China, test the ability of the US to cut off its trade routes, discover China’s weaknesses and address them with minimal internal opposition, and root out those who are too corrupt or too disloyal. There are some things that China will not discover about its vulnerabilities except from a crisis. This is one lesson Xi would have taken from Russia’s invasion of Ukraine.

Taiwan Attack Scenario

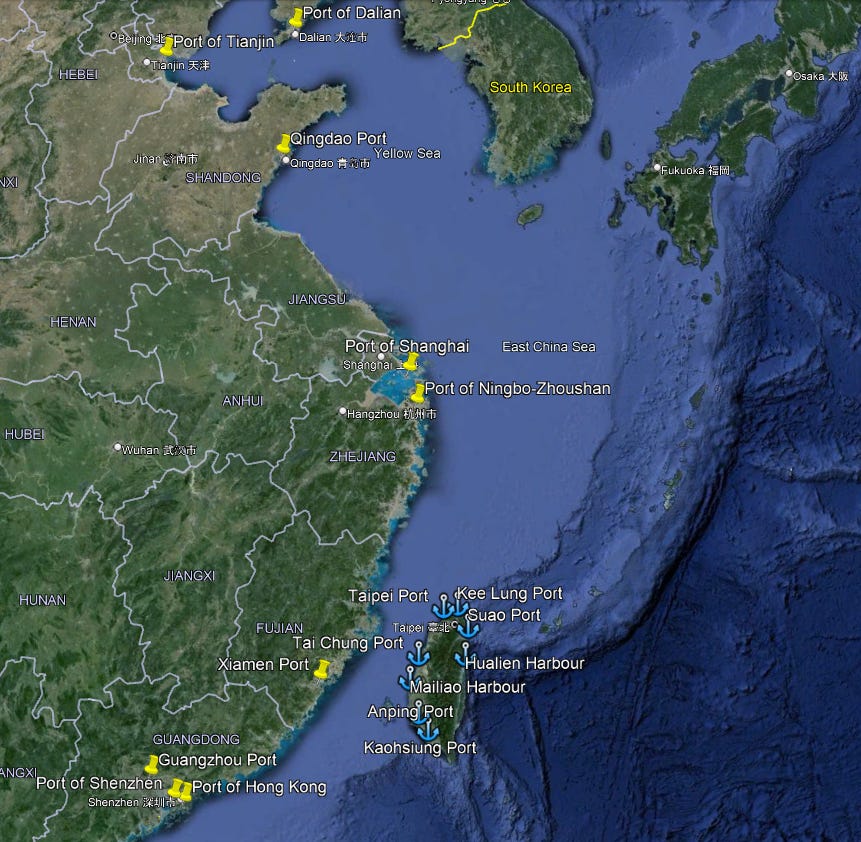

Note that China does not need to invade Taiwan directly and fight its way through the country. Taiwan relies on importing 1 million barrels of oil per day for the country to function, as well as vast quantities of food. It has 8 major ports. All China needs to do is to restrict Taiwan’s ports through a series of attacks on key infrastructure and through tactics short of direct attacks intended to stop shipping (blockades, threats, boardings to inspect ships, seizures, etc…), most likely with some signalling attacks.

China would want to allow only basic humanitarian goods rather than permitting free trade. China can do this by attacking Taiwanese port infrastructure and then by declaring a blockade. Taiwan would likely respond to a blockade by attacking Chinese naval assets, probably including regular civilian shipping. China would react with missile and drone strikes intended to neutralise firing locations. There can be a long aerial, naval and missile conflict before amphibious landing ships are deployed. China may well bet that it can deplete the West’s economy, and its ability to arm Taiwan, before invading. (To discuss the impact on shipping or aviation in more detail, please respond to this email or contact Firas Modad on LinkedIn).

Western reaction

The US is unlikely to target the Chinese mainland, or Chinese trade, as China is able to impose deterrence and prevent that. Taiwan may do so, but any anti-ship missiles it uses against civilian ships would be needed to target military vessels.

That said, the US has likely limited supplies to Ukraine, and its escalation against Iran, in order to preserve its ability to confront China. As such, the US may target some Chinese navy ships dedicated to enforcing a blockade on Taiwan or to landing an invasion force in Taiwan. This would likely result in Chinese attacks on US bases in Japan, South Korea and/or the Philippines. Both sides would want to keep the fight off their own heartland/mainland, as a means of avoiding nuclear escalation. Initially, it is likely that the various sides would seek to avoid targeting civilian shipping, as attacks on these can escalate into an all-out war on civilian shipping. It is unclear for how long such reasoning would hold.

Korea

We do not claim to understand the military balance of power in the Korean Peninsula, nor do we know how it will evolve in the aftermath or ahead of a Taiwan conflict. We are developing our source and analyst network to do so. We do note that Kim Jong Un has become increasingly committed to fighting South Korea, and that a Taiwan conflict will both present an opportunity to target South Korea and a challenge that, should the US prevail, North Korea would be dramatically weakened. The more South Korea gets drawn into the defence of Taiwan, and the greater its defence build-up, the more likely Kim is to escalate. By contrast, the more South Korea chooses neutrality, or the more it continues trading with China, the greater the likelihood that South Korea will drift out of the Western orbit and align with the Iran – Russia – China axis. We invite our clients to consider the North Korea wildcard when they think about Taiwan.

Commercial Impact:

Sanctions

We assess that the US would impose sanctions on China as severe as those imposed on Russia, and that Brussels would follow suit. The Russia and Iran crises have demonstrated that the EU is incapable of independent action.

China will likely respond with countersanctions, intended to weaken the West further, limit its manufacturing ability and impose a new global compromise that accords China a much greater say in international affairs. A key Chinese priority would be the expropriation of China-based, Western-owned manufacturing assets.

Sanctions on China would trigger severe inflationary pressure in the West. This would occur at a time when Western debt levels are extremely high, especially in the UK and the US, and with severe constraints on the ability of central banks to raise interest rates, as higher interest rates would impose a fiscal squeeze on governments.

Supply chains

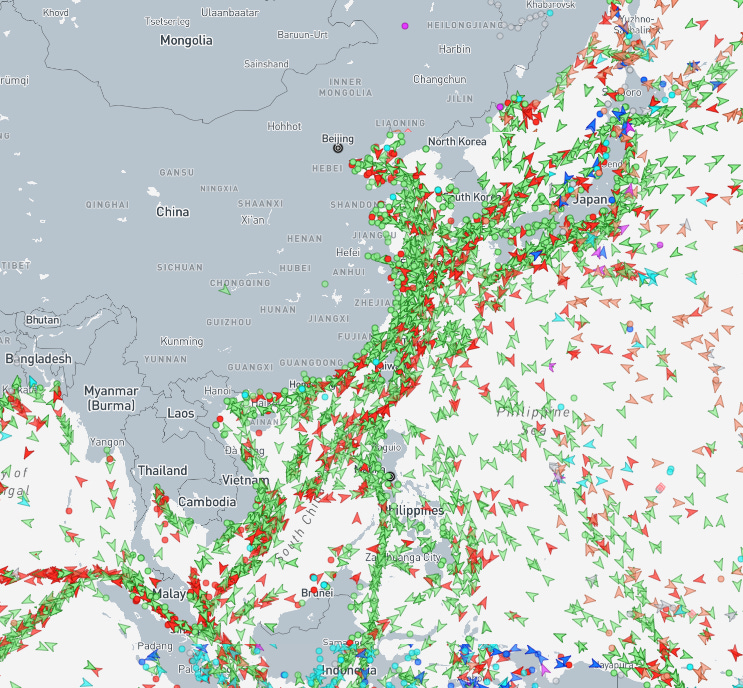

Supply chains from Asia would get disrupted due to US sanctions against China and against companies doing business with China, as part of a campaign to force countries to pick a side.

Furthermore, a conflict over Taiwan would threaten all trade going into China, South Korea and Japan, potentially forcing ships to divert traffic to longer routes, adding considerable cost and delays.

Obviously, if North Korea joins the fray, then the impact on Japanese and South Korean supply chains would be severe, as North Korea would use its missile forces to strike ports, ships and industrial hubs.

Sanctions on China would be extremely disruptive to the global financial and physical trade systems. 29% of all global manufacturing happens in China, with no one able to compete with that volume.

Sanctions on China may end up backfiring, as the sanctions on Russia did, and leading to a greater concentration of manufacturing power in China, or in countries friendly to China. Western manufacturing would be undermined with Western exports falling, as China would have access to cheap Russian food and energy, which the West has sanctioned itself away from.

ESG considerations would have to be thrown out the window to allow the West to develop cheap food and energy sources, but the ESG ideology is too ingrained in the minds of the current Western ruling classes.

As such, Western supply chains are more likely to be disrupted than their Chinese counterparts, and inflation in the West is likely be greater.

In any conflict, China’s economy would continue operating, albeit with more production shifting to war needs. Due to China’s industrial prowess, and its ability to prevent any dissent, it would be able to adapt more easily than the West.

By contrast, disruption to Taiwan’s economy, including its microchip exports, and to Western supply chains reliant on China, could be long lasting, given the West’s extreme dependence on imports from China. Furthermore, the US would likely sabotage TSMC to prevent its technology and capabilities from falling in Chinese hands.

In a conflict, China would likely prioritise expanding rail connections across Asia, as part of the Belt and Road Initiative, giving its industries access to maritime trade routes that bypass the conflict area. However, nothing can compare to shipping in terms of volumes transported and economies of scale.

Currency and trade

China may well devalue its currency, relying on the large stockpiles of commodities that it has built up, in order to ensure that it has a more favourable position than the West in global trade.

It is unimaginable that Africa, Latin America, the Middle East or most of Asia can do without Chinese imports of consumer goods. If forced to choose, they may choose closer ties to China. This will mean that they will find ways to continue trading with China regardless of the threat of sanctions.

The US can have the global reserve currency, or it can sanction the world’s largest food and energy producer and the world’s largest manufacturer. There will come a point after the Taiwan invasion where the US dollar’s pre-eminence is severely threatened.

As inflation in the West surges, the world may end up in a dual system, where, in the West, a rapidly inflating dollar still reigns, while, in the rest of the world, a combination of the yuan, rouble and barter reign.

Countries like the UAE, Türkiye, Morocco, Malaysia, Indonesia, Georgia, Lebanon, South Africa, etc… which can trade with both China and the West, stand to profit from being middlemen, helping the two blocs to continue trading with one another.

Western politics

For the West, the combination of high debt, high interest rates, high migration, and high inflation is by its very nature politically destabilising. The current crop of Western political parties, which mostly offer different versions of managed decline, will not survive, nor will they exit without a fight. This will cause multiple countries to experience political and/or constitutional crises.

Most of the impact of a Taiwan China conflict would stand under any administration. But, under a Biden administration, it may well be easier for the collective West to act with less hostility between the EU and the US. Under a Trump administration, the US can be relied on to boost the volume of energy exports, helping European economies somewhat.

Winners: Arms manufacturers; Nvidia, Intel and other leading Western technology manufacturers; manufacturers who export to the West and whose supply chains are dependent on Türkiye, Morocco, Latin America, Pakistan and India; discount retail chains in the West.

Losers: Western-based manufacturers and importers who depend on South Korea, China or Japan; vehicle manufacturers dependent on microchips from Asia; retailers and brands targeting the Western middle class and upper middle class.

Excellent analysis and overview of the potential scenario for conflict in East Asia and its global impact. But one question, who are you referring to exactly when you speak of “dissident oligarchs”? The likes of Aven and Friedman are gone from Russia (as far as I am aware). And anyway, it’s been well over a decade since Russia had any billionaire who could actually be classified as an “oligarch”. The term doesn’t really fit Russia’s political reality as the center of power has long been in the hands of the siloviki, who have long been Putin’s inner circle.